Energy markets are beginning to value Bitcoin mining that may change on and off as a grid service.

Curtailment stays elevated in areas with excessive renewable penetration, and quick shortage bursts proceed to set worth for quick demand discount, which creates room for load that soaks noon surplus and idles throughout tight hours.

In keeping with the California Impartial System Operator, 179,640 megawatt-hours (MWh) of wind and photo voltaic power have been curtailed in September 2025. Market knowledge in Europe and Asia present wider home windows of damaging or low daytime costs, which strengthens the case for versatile demand to enhance storage and transmission buildouts.

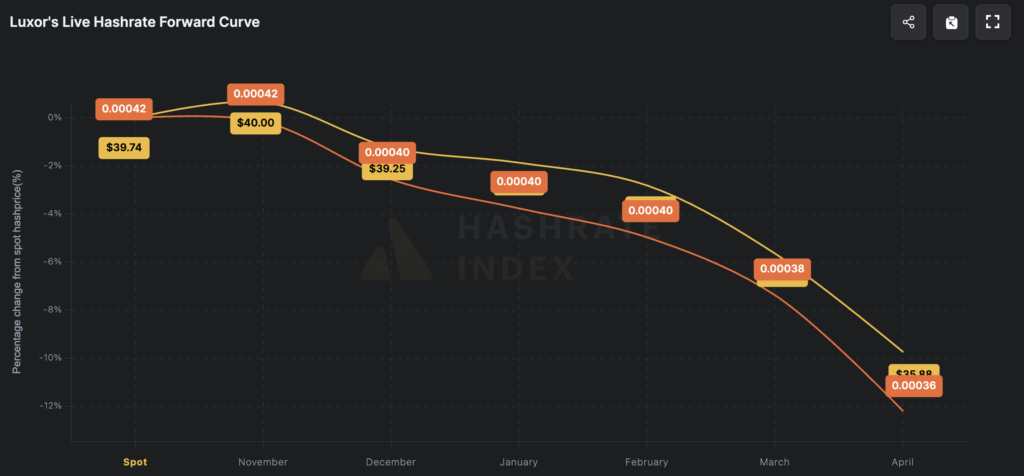

Even after the latest crash, as we speak’s spot hashprice is roughly $39/PH/day, and mining income continues to exceed typical energy prices for well-managed fleets utilizing environment friendly {hardware} and beneficial energy contracts.

This means the financial lane for demand-response (i.e., flexibly scaling operations round energy pricing) stays open relatively than closing.

That stated, fleets with larger energy prices or much less environment friendly machines will face tighter margins, particularly given the latest drop in BTC costs.

In keeping with Hashrate Index, the six-month ahead common is predicted to dip to round $35 by April subsequent 12 months.

Extra intuitively, a 17.5 J/TH machine attracts roughly 17.5 kW per PH. Which means every PH consumes about 0.42 MWh per day, so a $39 hashprice equates to roughly $93/MWh in gross income.

That breakeven band units the “max value to run” (earlier than accounting for ancillary funds or hedging methods which will justify operating above that stage.)

Masses can run beneath the edge and may promote flexibility or change off above it.

To make the comparability express, the desk beneath reveals a simplified view of miner gross income per MWh throughout two reference hashprices at a typical fashionable effectivity.

After accounting for typical website overhead, cooling losses, and pool charges, the sensible cutoff for a lot of miners is nearer to $70–$85 per MWh. Above that band, fleets start shutting down except they’ve unusually environment friendly {hardware} or hedged energy.

Versatile load just isn’t solely an power purchaser, but it surely will also be a reliability product.

ERCOT permits certified Controllable Load Sources to take part in real-time and ancillary markets, paying the identical clearing value as era for Regulation, ECRS, and Non-Spin companies.

That framework pays mines for quick load reductions throughout shortage along with the prevented value of not operating at excessive costs. ERCOT’s market design retains shortage occasions sharp however bounded, with a system-wide provide cap at $5,000 per MWh and an Emergency Pricing Program that lowers the cap to $2,000 per MWh after 12 hours on the excessive cap inside 24 hours.

This preserves acute value indicators whereas limiting tail danger, which helps the economics of price-responsive curtailment.

Coverage is shifting from permissive to efficiency primarily based, and Texas is the check case. Texas Senate Invoice 6, enacted in 2025, directs PUCT and ERCOT to tighten interconnection and require participation in curtailment or demand administration for particular giant a great deal of 75 MW and above, and to overview netting when giant hundreds co-locate with era.

In keeping with McGuireWoods, rulemakings are underway, and the route is towards clearer expectations for response functionality, telemetry, and interconnection staging. Baker Botts notes that behind-the-meter netting and generator–load co-location will draw added scrutiny, which issues for websites paired with fuel peakers that search speedy curtailment and sooner interconnection timelines.

The sensible response could also be modular footprints and staged buildouts that both stay beneath the statutory threshold or deploy capability in tranches with express demand-response commitments.

Operations may even change as market plumbing evolves. ERCOT plans to maneuver real-time to RTC+B on Dec. 5, 2025, which improves dispatch granularity and may profit quick load that may comply with sub-hourly indicators.

Potomac Economics has documented how ORDC shortage adders and temporary real-time spikes focus a big share of economics right into a small set of hours. That’s the place controllable demand can earn by dropping when costs climb and by promoting ancillary functionality throughout the remainder of the day.

The worldwide image factors in the identical route.

Japan’s renewable curtailments rose 38% 12 months over 12 months to 1.77 TWh within the first eight months of 2025 as nuclear restarts lowered flexibility.

China’s first-half 2025 curtailment charges climbed to six.6% for photo voltaic and 5.7% for wind as new builds outpaced grid integration. Gridcog’s evaluation reveals the unfold and depth of damaging costs throughout European noon hours, reinforcing that the “duck-curve dividend” is now not a California-only characteristic.

In america, wholesale averages pattern larger in 2025 in most areas, but volatility persists. That leaves worth in price-responsive curtailment even the place energy-only averages seem tame.

Undertaking archetypes replicate these incentives. A roughly 25 MW modular mining website powered by flared fuel reached full energization in April 2025, in response to Information Middle Dynamics, illustrating a waste-to-work pathway that converts in any other case flared fuel into energy for curtailable demand.

CAISO’s recurring noon curtailment strengthens the case for renewable co-location with load that runs by means of surplus hours and idles at night peaks. Fuel-peaker co-location stays related in markets with speedy ramping wants, though SB6 requires initiatives to plan for telemetry and netting necessities throughout interconnection.

{Hardware} and environmental coverage form the capex and off-grid thesis from one other angle. The USA doubled Part 301 tariffs on sure Chinese language semiconductors to 50% in 2025, elevating the prospect that ASIC import prices rise materially relying on classification.

The Inflation Discount Act’s Waste Emissions Cost for methane ramps from $900 per ton in 2024 to $1,200 in 2025 and $1,500 in 2026, though implementation has been contested. Regional hashrate placement will replicate these cross-currents.

Cambridge’s 2025 business report reveals america as the middle of gravity, with surveyed corporations representing almost half of implied community hashrate.

New ultra-large websites in ERCOT face larger course of overhead and express efficiency obligations, which might steer incremental development towards modular builds, SPP and MISO South, Canada, or off-grid fuel till interconnection timelines and rule readability catch up.

For miners and grids, the maths is easy, then the main points matter.

Income per MWh is a perform of hashprice and effectivity, so the run-price threshold strikes with Luxor’s curve and fleet combine.

Uptime turns into a alternative variable, not a constraint, so long as curtailment aligns with high-price intervals and ancillary capability gives are certified and dispatched.

The operational playbook is to submit load as a controllable useful resource, earn when the grid is tight by dropping, and run when power is reasonable sufficient to beat the marginal run value.

In markets the place noon surplus is routine, curtailment stops being waste and turns into the runway for demand that may be dispatched like era.