BITF has taken off and the momentum isn’t fading. Is there a growth the market’s quietly pricing in? Or is it time to re-rate the inventory altogether?

The next visitor submit comes from BitcoinMiningStock.io, a public markets intelligence platform delivering knowledge on corporations uncovered to Bitcoin mining and crypto treasury methods.

Bitfarms Inventory Surges – Re-Score Section Subsequent?

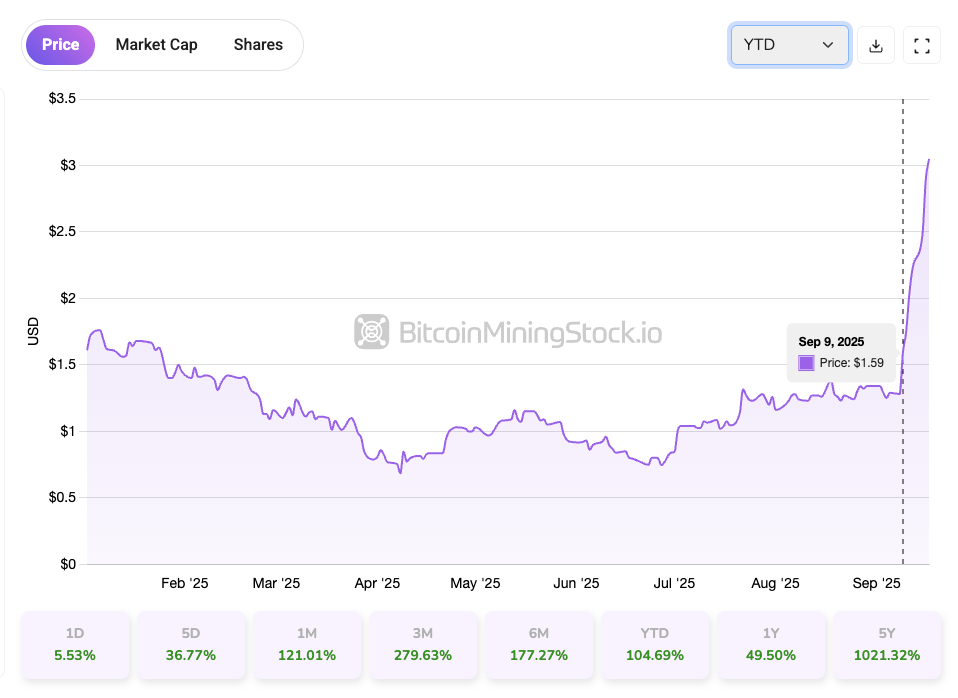

Bitfarms (Nasdaq: BITF) closed final week because the top-performing Bitcoin mining inventory tracked by BitcoinMiningStock.io, posting a shocking 72.86% acquire over a 5-day buying and selling interval. The rally started round September ninth and reveals little signal of slowing on the time of writing. Notably, this run-up occurred within the absence of any firm information launch bulletins. As a substitute, investor sentiment appears to have been pushed by a renewed understanding of Bitfarms’ enterprise transformation, amplified by CEO Ben Gagnon’s presentation on the H.C. Wainwright twenty seventh Annual International Funding Convention.

Whereas the presentation wasn’t broadly broadcast, investor dialogue on X picked up tempo and social feeds turned noticeably extra bullish on BITF. For these conversant in my December 2024 report, this marks a shift. Again then, I wrote:

“Whereas Bitfarms’ monetary and operational methods are aligned with trade traits, the corporate struggles to face out because of an absence of a transparent, distinctive aggressive benefit.”

9 months later, it appears that evidently the corporate has discovered an edge – to grow to be a North American vitality and compute infrastructure firm. And this evolving technique is lastly getting investor consideration.

So I need to return to the basics of Bitfarms’ current developments, and decide whether or not it’s time to re-rate the inventory.

What Bitfarms’ CEO Stated on the H.C. Wainwright Convention

On the H.C. Wainwright occasion, Gagnon positioned Bitfarms as a future “North American vitality and compute infrastructure firm.” He framed the corporate’s 18 EH/s Bitcoin mining operation as a “low-cost bridge financing software” to help its transition into HPC and AI infrastructure. Whereas mining nonetheless covers all working bills and contributes to capex, no additional miner purchases or fleet expansions are deliberate. As a substitute, the present fleet, benefiting from low-cost electrical energy and excessive operational effectivity, is predicted to generate steady free money circulate by means of 2026 below most BTC pricing eventualities. In brief, Bitfarms intends to unlock the potential of its vitality portfolio, as soon as constructed to help mining, to serve the rising HPC/AI market.

Bitfarms’ geographic footprint has additionally shifted to help this technique. When Gagnon turned CEO, simply 45% of the corporate’s footprint was in North America. In the present day, that quantity stands at 82%, with almost all future development concentrated within the U.S. The eventual exit from Latin America, significantly Argentina, by November 11, 2025, marks a decisive pivot towards changing into a U.S.-focused platform.

Screenshot from Bitfarms presentation.

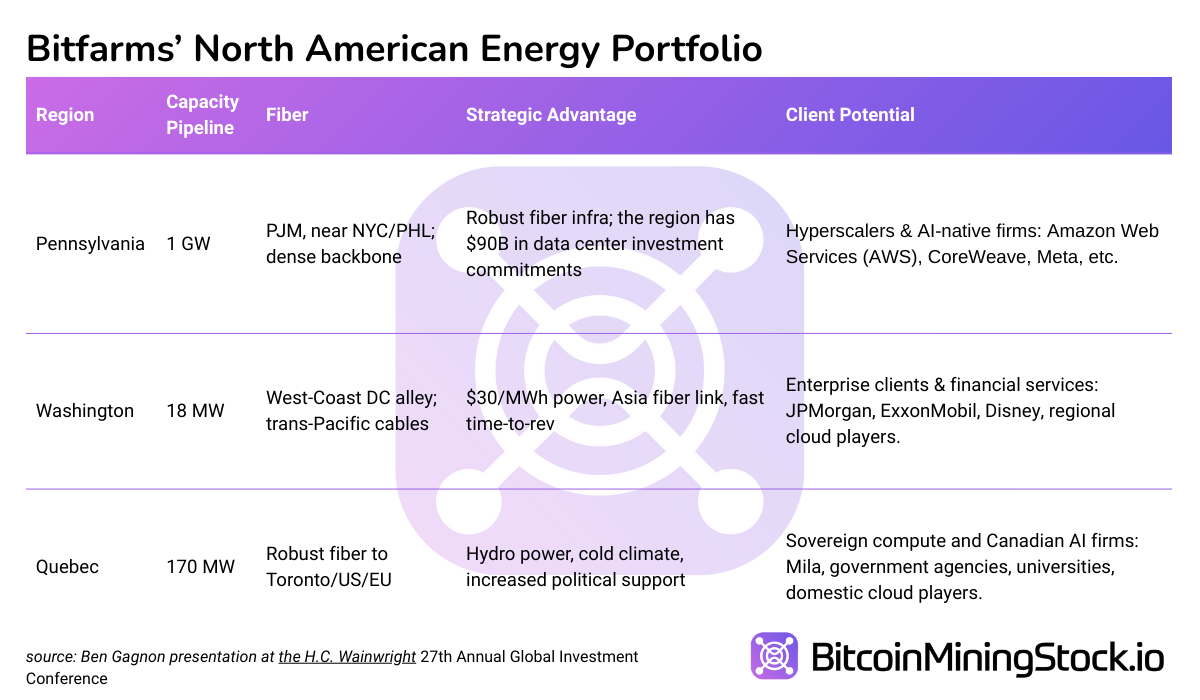

In North America, the corporate now has a 1.2 GW energy pipeline. Key websitesembody Panther Creek in Pennsylvania, its established operations in Quebec, and a rising footprint in Washington state. These websites are situated close to main fiber optic corridors, enabling them to help knowledge middle workloads throughout North America and doubtlessly throughout the Atlantic. With favorable energy economics and improved Energy Utilization Effectiveness (PUE), Bitfarms believes it may possibly ship larger compute yields per megawatt which provides a crucial edge in HPC markets.

This evolving narrative of mining immediately, infrastructure tomorrow, is aligned with investor sentiment. Markets are exhibiting a transparent desire for long-term, steady income from AI infrastructure internet hosting.

Bitfarm’s HPC Improvement: Hype or Actual Progress?

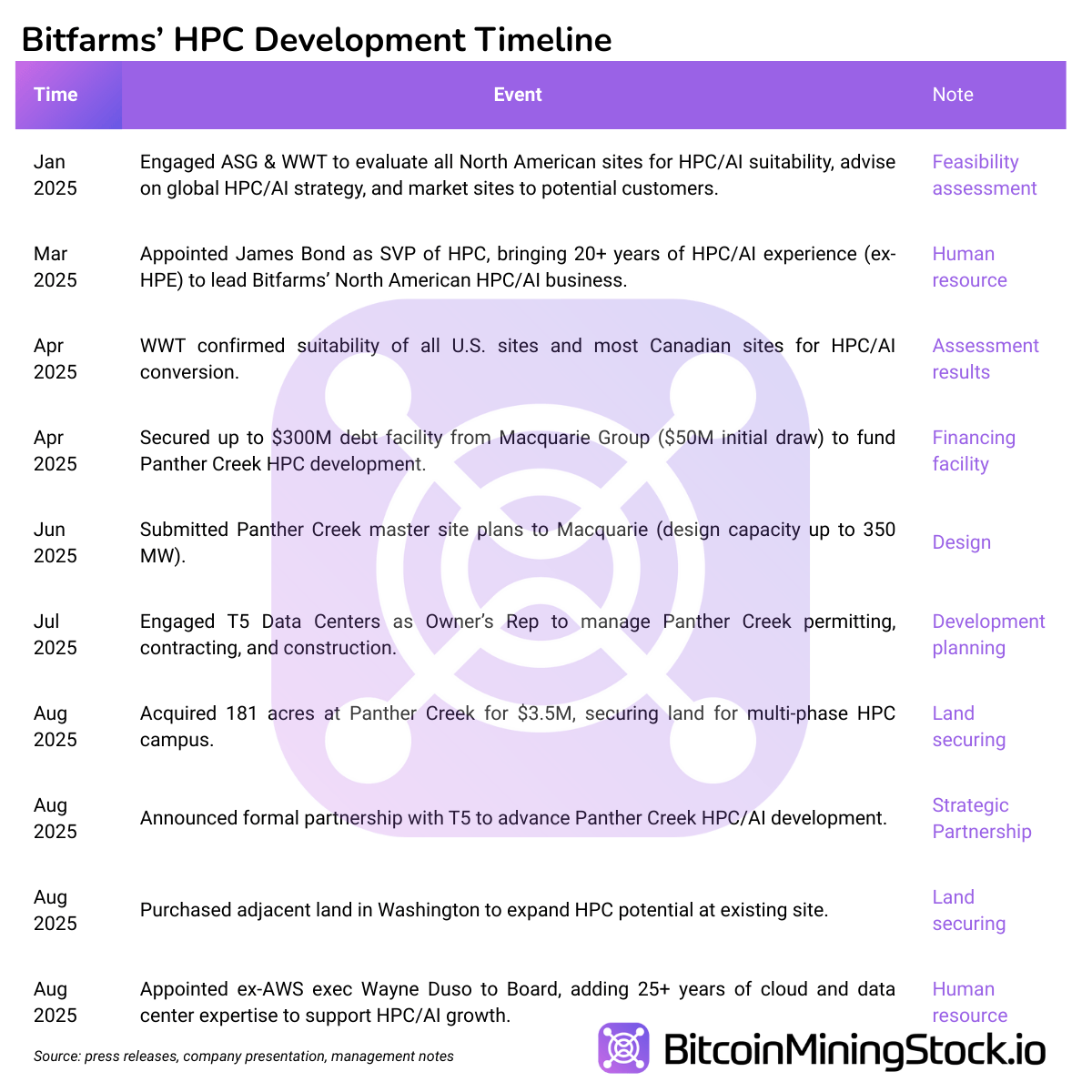

Bitfarms’ HPC growth is starting to take tangible form, although it stays within the early phases. Over current quarters, the corporate has initiated site-level feasibility assessments, secured permits and capability, strengthened its group with related experience and established strategic partnerships to market the websites to potential clients.

To the shock of many, even the long-criticized Stronghold acquisition, as soon as deemed as overpriced, has turned out to be a strategic asset. The acquisition supplied Bitfarms with a big, scalable footprint in Pennsylvania, an rising hub for AI and HPC knowledge middle growth. This will increase the possibilities of the corporate to draw future AI and HPC shoppers.

In reality, Pennsylvania, a part of the PJM interconnection, is now Bitfarms’ main area for AI/HPC buildout (the corporate has a 1 GW vitality pipeline there). In accordance with its newest investor presentation, Bitfarms is positioned to fulfill surging HPC and AI demand with coast-to-coast infrastructure: east (Pennsylvania), west (Washington) and north (Quebec).

Screenshot from the Bitfarms’ presentation.

Collectively, these fiber linked websites allow Bitfarms to serve latency-sensitive workloads on each U.S. coasts and hyperlink them with Europe. This networked structure is a key differentiator as the corporate pivots towards HPC infrastructure.

The next desk summarizes the traits of every area:

In brief, Bitfarms has laid significant groundwork for its HPC and AI pivot, however the initiative stays firmly within the pre-commercial part. The subsequent few quarters will probably be crucial in figuring out whether or not this technique matures right into a scalable income engine, or as a substitute turns into a capital-intensive distraction that strains the steadiness sheet with out near-term payoff.

Financing the Pivot

Bitfarms is financing its transition to HPC by means of a mixture of inside money circulate, asset optimization, and a brand new credit score facility. Its 17.2 EH/s mining fleet generates ~$8M/month FCF below the present market. Administration continues to promote Bitcoin to fund capex and opex whereas nonetheless holding 1,005 BTC on their steadiness sheet. Bitfarm’s exit in Argentina by November 11, 2025 will unlock roughly $18 million by means of lease releases, legal responsibility reductions, and the sale of just lately imported S21+ miners.

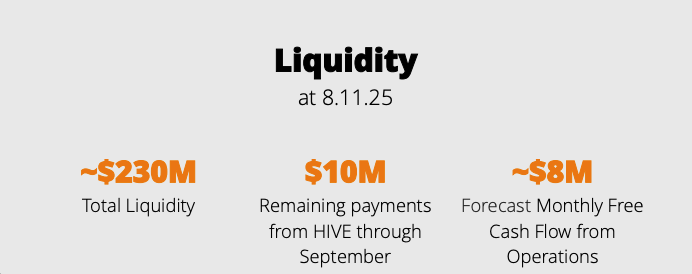

As of August 11, the corporate held ~$230 million in liquidity (money plus unencumbered BTC), with a further ~$10 million anticipated from the Yguazu/HIVE sale and pending miner gross sales.

Bitfarms Liquidity Place (screenshot from the firm presentation).

As well as, Bitfarms secured a as much as $300 million credit score facility from Macquarie to fund its Panther Creek web site. The primary $50 million has been drawn to help early growth, with the remaining $250 million out there in tranches tied to building milestones. Upon activation, the construction converts to non-recourse mission debt. The ability carries an 8% rate of interestand consists of warrant protection, $25 million minimal money necessities, and BTC-price-linked covenants. The subsequent tranche is predicted in This fall 2025, contingent on allowing progress.

Whereas such a funding construction preserves flexibility and limits dilution, it has a timing hole to handle. HPC income stays quarters away (doubtlessly mid-2026 or later). In the meantime, friends like Core Scientific, TeraWulf, Utilized Digital are already onboarding shoppers. Execution pace, price management, and buyer acquisition will probably be crucial to closing the hole.

Ultimate Ideas

Bitfarms is actively pivoting from a world Bitcoin miner to a North American vitality and compute infrastructure firm. Its U.S. websites are close to main fiber traces, giving them the technical viability to help AI internet hosting workloads from coast-to-coast* and even, hypothetically, to Europe because of low energy prices and favorable geolocation.

*Whereas “coast-to-coast” attain sounds compelling, some grounded perspective is required: Bitfarms’ West Coast presence in Washington solely has 18 MW of capability, which is nicely under the everyday 100+ MW measurement seen in earlier HPC colocation offers. Its North (Quebec) websites, whereas sizable, are topic to regulatory approval earlier than being repurposed for HPC workloads. That leaves the East (Pennsylvania), with websites like Panther Creek, as the corporate’s solely HPC-ready asset with clear roadmap for now.

That stated, the transition is early. The corporate has but to have any function constructed knowledge middle prepared or land a fabric HPC deal. Till then, a lot of the upside stays aspirational. However insider habits provides some confidence: the corporate initiated a share buyback program and CEO Ben Gagnon has elevated his private holdings.

For buyers with a 12-24 month horizon and urge for food for early-stage infrastructure development at deep-value entry factors, Bitfarms might now current an asymmetrical alternative. Its developments, from senior hires to fiber-ready properties and staged financing, provide tangible causes to revisit the thesis.

In the end, it’s your name whether or not to re-rate the inventory. But when Bitfarms delivers on even a part of its infrastructure narrative, the upside case may look fairly completely different from the everyday Bitcoin mining play.